全球交易商监管查询APP

什么是WikiFX

DBG Markets: Market Report for Oct 31, 2025

摘要:Dollar Dominates as Global Policy Divide; Gold Holds Ground Ahead US GDPMacro Focus: Trump–Xi Meeting Trade De-escalationOn the geopolitical front, investor sentiment turned risk-on following signs o

Dollar Dominates as Global Policy Divide; Gold Holds Ground Ahead US GDP

Macro Focus: Trump–Xi Meeting & Trade De-escalation

On the geopolitical front, investor sentiment turned risk-on following signs of easing U.S.–China trade tensions. The highly anticipated meeting between President Trump and President Xi Jinping at the APEC Summit ended without a major breakthrough but achieved a notable de-escalation of trade risks.

· One-Year Truce: Both leaders agreed to a 12-month suspension of their tariff conflict, pausing all new measures, including China‘s proposed rare-earth export restrictions and Washington’s counter-tariff plans.

· Tariff Adjustments and Agricultural Purchases: President Trump announced a tariff reduction on Chinese goods tied to fentanyl controls from 20% to 10%, while China pledged to resume large-scale U.S. agricultural imports, including soybeans, and strengthen cooperation on fentanyl enforcement.

Markets interpreted the outcome as a temporary geopolitical reprieve, supporting equities and the U.S. Dollar, while reducing safe-haven demand for Gold.

Dollar: Undoubtedly the Winner

Amid a week dominated by central bank decisions and trade de-escalation, the U.S. Dollar emerged as the clear outperformer. Renewed confidence in the greenback has driven strong gains against major peers, including the euro and the Japanese yen, as highlighted in our earlier daily commentary.

USD Index, H4 Chart

With the US Dollar now holding firmly above the 98.50–99.00 support zone, the technical bias remains to the upside. A sustained move above this range opens the door for a potential retest of the August high near 100.00, marking the next key resistance level to watch in the near term.

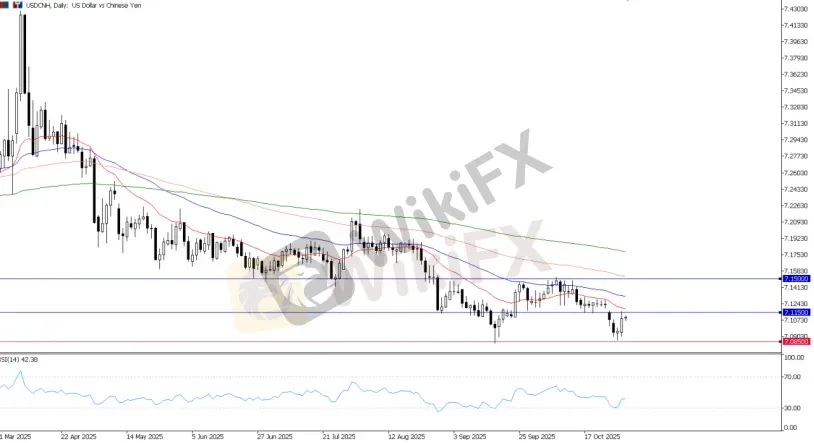

USD/CNH Analysis: Technical Rejection & Range Watch

The offshore Chinese yuan (CNH) remains highly sensitive to both U.S. Dollar momentum—as reflected in the DXY rally—and the evolving geopolitical narrative following the Trump–Xi engagement. The Dollars surge past the 99.00 level has placed renewed upward pressure on USD/CNH, prompting CNH weakness across the board.

USDCNH, Daily Chart

Recent price action shows a decisive breakdown from the prior consolidation range between 7.1500 and 7.1150, before finding temporary support near 7.0850, a level aligned with the previous local low.

The short-term technical outlook is cautiously bearish following this breakdown. However, the combination of a strong Dollar and easing trade tensions could provide a soft floor for the pair around current levels.

USDCNH, H2 Chart

On the topside, if the DXY rally extends, particularly in response to the strong U.S. GDP print, renewed buying momentum could emerge. A sustained reclaim and close above 7.1150 would invalidate the current bearish bias, opening the path toward 7.1300 and the upper consolidation boundary near 7.1500.

Conversely, a failure to hold above 7.1150 would reinforce downside pressure, with next weeks U.S. labor data and potential recalibration of Dollar expectations acting as catalysts for further weakness.

Conclusion: The near-term focus remains on whether the recent rebound can push the pair back above 7.1150. Sustained strength above this level likely requires a fresh fundamental trigger, most likely from stronger-than-expected U.S. economic data or continued Dollar momentum.

Gold Finds Support Despite Yield and Risk-On Surge

Gold prices managed to stabilize and rebound on Thursday, holding firm around the $3,900–$4,000 zone, despite two typically bearish forces: rising U.S. Treasury yields and a broad risk-on rally following the U.S.–China trade truce. This resilience suggests that gold may be attempting to establish a short-term bottom near current levels.

XAU/USD, H2 Chart

From a technical standpoint, gold continues to hold firm within the $3,900–$4,000 support area, where repeated intraday rebounds suggest the formation of a potential short-term base. Price action indicates a period of tight consolidation and contained volatility is likely ahead.

The short-term ascending channel remains intact, with $3,950 acting as immediate intraday support. However, upside potential appears limited in the current macro environment, as two of golds primary drivers — safe-haven demand and monetary easing expectations — have both weakened.

Conclusion: Golds near-term direction hinges on the upcoming U.S. GDP report.

· A weaker print (below 3.0%) may trigger Dollar softness and renewed Fed easing bets, potentially lifting gold back above $4,000.

· Conversely, a strong GDP figure would reinforce Dollar strength and rising yields, likely keeping gold range-bound or pressuring it back toward $3,900.

Bottom Line

Heading into the U.S. GDP release, the Dollar remains the market‘s preferred play — while gold’s resilience near $3,900–$4,000 suggests a tentative floor, pending confirmation from upcoming data.

免责声明:

本文观点仅代表作者个人观点,不构成本平台的投资建议,本平台不对文章信息准确性、完整性和及时性作出任何保证,亦不对因使用或信赖文章信息引发的任何损失承担责任

天眼交易商

热点资讯

美国政府开门遥遥无期或令“非农”继续泡汤 下周汇市仍有重磅

WikiFX

WikiFX外汇天眼发布:10月客户投诉黑榜单TOP10

WikiFX监管变动预警:这些外汇平台被监管撤销牌照!

WikiFX汇率计算

CNY

USD

当前汇率: 0

请输入金额

CNY

可兑换金额

USD

开始计算